The page you were trying to view is not available for your role.

Our market summary

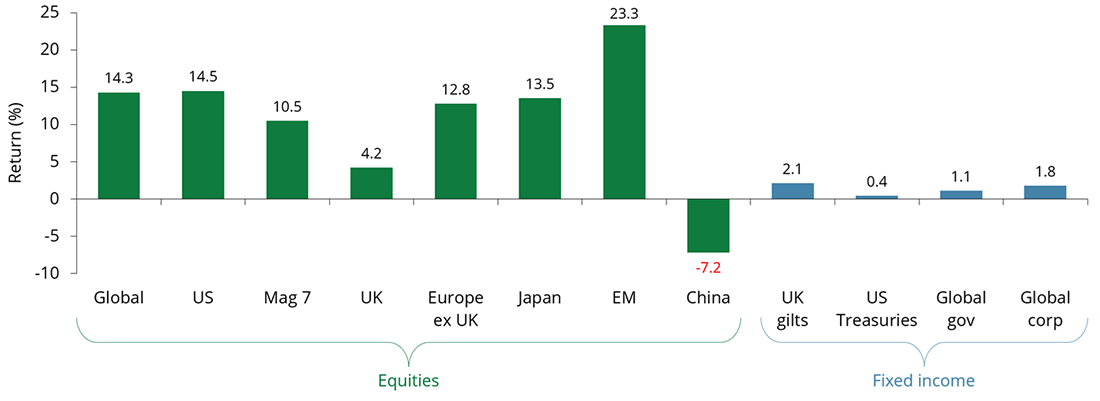

The second quarter of 2026 marked a sharp turnaround for investors. Markets recovered strongly as tensions in the Middle East eased and concerns about energy supply disruption faded. Falling oil prices helped reduce inflation pressures, while enthusiasm surrounding artificial intelligence (AI) and continued investment in technology infrastructure boosted investor confidence. Corporate earnings remained resilient and economic conditions proved more supportive than expected. Global equities delivered strong gains, up 14.3%, led by technology and emerging markets, while commodity prices declined.

Equity markets

US

US

US equities delivered a strong rebound during the quarter, up by 14.5%, supported by robust corporate earnings, resilient economic growth, and continued optimism around AI. Investors remained focused on companies benefiting from spending on data centres, semiconductors, and cloud infrastructure. As confidence improved, gains broadened beyond the largest tech companies into more cyclical sectors, while more defensive areas of the market lagged.

Europe

Europe

European equities were up 12.8% as improving investor sentiment, easing energy prices, and resilient company earnings supported performance. However, Europe’s lower exposure to the technology sector meant the region benefited less from the AI-driven rally. Industrial and financial companies performed well as confidence in economic growth improved. More defensive sectors lagged as investors favoured areas offering greater earnings growth potential.

UK

UK

UK equities were up 4.2% but underperformed other developed markets. The UK’s limited exposure to technology companies meant it benefited less from the resurgence in AI-related investment. Falling commodity prices also reduced support for the energy and mining sectors that had performed strongly earlier in the year. Nevertheless, improving global risk appetite and resilient corporate earnings helped underpin returns.

Japan

Japan

Japanese equities performed well during the quarter, up 13.5%, supported by improving investor sentiment and strong demand for technology-related businesses. Companies linked to semiconductor supply chains benefited from continued investment in AI. Export-oriented businesses were also supported by healthy global demand. Strong corporate profitability and improving confidence in economic prospects also helped drive returns higher across the market.

Emerging markets

Emerging markets

Emerging market equities were the strongest-performing asset class in the quarter with a return of 23.3%. Markets with significant exposure to semiconductor manufacturing and technology hardware, particularly in Asia, benefited from renewed investor enthusiasm for AI-related growth. South Korea and Taiwan performed especially well as demand for advanced chips and technology infrastructure remained strong. Improving global risk appetite also supported returns.

Fixed Income

Emerging markets

Fixed income markets delivered modest positive returns, although performance varied across regions. Falling energy prices helped ease inflation concerns and supported investor confidence. Corporate bonds outperformed government bonds as stronger economic growth and resilient company earnings led credit spreads to tighten. Government bond markets were more mixed as investors assessed the outlook for inflation, growth, and interest rates.

Source: Quilter as at 30 June 2026. Total return, percentage growth over period 31 March 2026 to 30 June 2026. Equities are represented by the appropriate MSCI index, the Magnificent Seven is represented by the Roundhill Magnificent Seven ETF, UK gilts is represented by the ICE BofA UK Gilt Index, US Treasuries is represented by the ICE BofA US Treasury (GBP Hedged) Index, global government bonds is represented by the Bloomberg Global Aggregate Government - Treasuries (GBP Hedged) Index, and global corporate bonds is represented by the Bloomberg Global Aggregate - Corporate (GBP Hedged) Index.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance.

Important Information

The value of investments can fall as well as rise. You might get back less than you invested.

This communication is issued by Quilter, a trading name of Quilter Investment Platform Limited.

Approver: Quilter July 2026

QIP 24035/20/17706

Marcus Brookes

Chief Executive Officer and Chief Investment OfficerMarcus is both the Chief Executive Officer and Chief Investment Officer of Quilter Investors. Marcus joined Quilter Investors in December 2021 from Schroders Personal Wealth, where he also held the role of Chief Investment Officer. Marcus has considerable investment management experience with a deep understanding of the multi-asset sector, having managed multi-manager fund ranges for more than 25 years at Schroders, Cazenove Capital, Gartmore, and Insight Investments.