This week’s blog is written by portfolio manager CJ Cowan

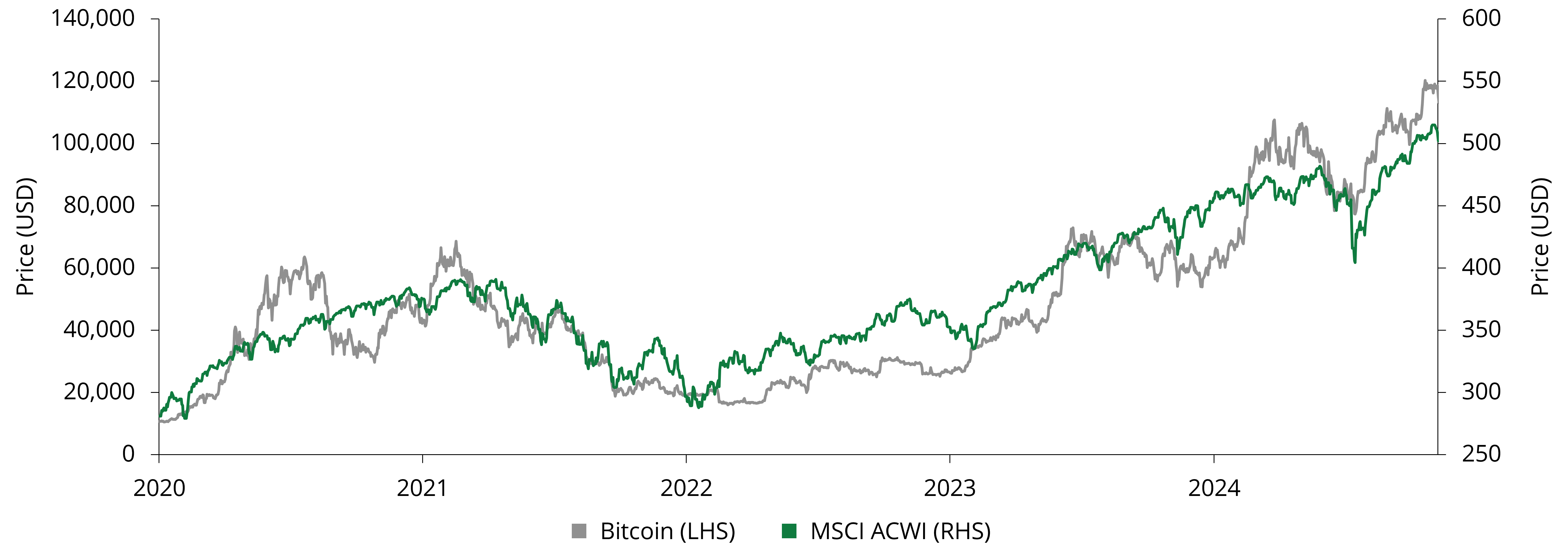

The mere mention of cryptocurrencies can be a triggering word for many, be they bitcoin evangelists who espouse that the current financial system is broken, or sceptics who claim it’s just a giant Ponzi scheme. A more measured assessment might be that cryptocurrencies deliver several benefits, such as rapid settlement of transactions, but for all the problems they solve, they create many new ones: cue stories of forgotten passwords for digital wallets with millions of dollars’ worth of bitcoin in them. As with most things, the right answer probably lies somewhere in the middle. We receive a lot of questions from clients asking about our views on crypto, so here’s a quick round-up of our thoughts.

As a disclaimer, this isn’t going to be a deep dive into why bitcoin may or may not replace fiat currency. We will take it as a given that bitcoin is a legitimate asset and consider it in the same way we would any other new asset class for inclusion in our portfolio.