In order to aid your understanding, the underlined terms are hyperlinked to definitions in our online investment glossary.

Our market summary

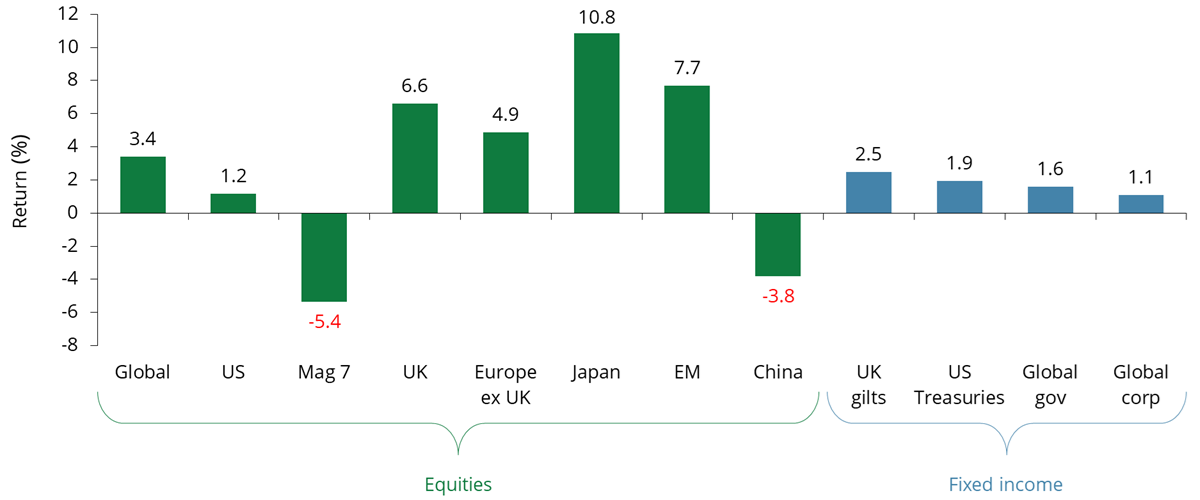

February was characterised by a clear shift in investor sentiment. Markets moved away from large US technology stocks, particularly those linked to artificial intelligence (AI), and towards a broader mix of regions and sectors. While headlines were dominated by geopolitical developments and legal challenges to US trade policy, economic data was generally supportive. Meanwhile, inflation pressures continued to ease across major economies, helping investors feel more confident about the outlook for interest rates. Equity markets outside the US performed better, while government bonds delivered positive returns as investors adopted a more cautious stance. Overall, the month continued to highlight the importance of diversification, with market leadership broadening beyond a small group of high‑growth stocks.

US

US

In February, US equities returned 1.2% for sterling-based investors. However, this gain was due to the strength of the dollar vs sterling rather than market performance. In US dollar terms, US equities actually declined by 0.9% as investors reassessed valuations in large technology companies. Despite strong earnings results, concerns grew about whether heavy spending on AI will deliver sufficient long‑term returns. As a result, growth stocks lagged, while more defensive and value‑oriented sectors such as utilities, materials, and consumer staples held up better. US small caps performed relatively well, supported by improving domestic growth expectations and their lower exposure to mega‑cap technology names. Overall, investors favoured companies with more predictable earnings and cash flows.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance.

Europe

Europe

European equities were up 4.9% in February, benefiting from improving economic data and a rotation away from US markets. Inflation continued to fall, reinforcing confidence that price pressures are under control and supporting expectations for a more stable interest‑rate environment. Energy and communication services stocks performed well, while healthcare and financials lagged. Elsewhere, business surveys pointed to gradually strengthening activity, particularly in manufacturing, and political uncertainty eased in France following agreement on the 2026 budget, which helped improve investor sentiment. Although technology stocks rose overall, software companies struggled as concerns grew about potential disruption from AI.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance.

UK

UK

UK equities performed strongly, up 6.6%, supported by the value‑focused sector mix of the UK market. Healthcare, utilities, telecommunications, and basic materials were among the best‑performing areas, with large pharmaceutical companies benefiting from solid earnings and corporate activity. Large‑cap stocks outperformed smaller, more domestically focused companies, reflecting ongoing caution around the UK growth outlook. Inflation slowed meaningfully during the month, increasing expectations that interest rate cuts may be approaching, even as economic growth forecasts were revised lower. Overall, the defensive characteristics of the UK, and exposure to income‑generating sectors, continued to appeal to investors seeking stability amid global uncertainty.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance.

Japan

Japan

Japanese equities were one of the strongest‑performing markets in February ending the month up by 10.8%. A decisive election result strengthened expectations for political stability and continued pro‑growth policies, boosting investor confidence. Market leadership broadened, with cyclical sectors and companies linked to domestic demand performing well. Businesses involved in AI infrastructure, such as semiconductor and optical component manufacturers, also delivered strong gains. In contrast, some software and IT companies lagged due to concerns about disruption from generative AI. Overall, optimism around economic momentum, policy support, and improving corporate governance underpinned strong performance.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance.

Emerging markets

Emerging markets

Emerging markets were up 7.7% over the month, significantly outperforming developed markets. The gains were led by Asian markets, particularly Korea and Taiwan, where technology hardware and memory‑related stocks benefited from improving earnings expectations. Strength in precious metals supported markets such as South Africa, while political developments boosted confidence in Thailand. Elsewhere, performance was more mixed. Brazil lagged the broader emerging market index as economic data pointed to slowing growth, while China underperformed due to weakness in internet‑related stocks. India delivered positive returns but trailed the index, reflecting concerns over higher government borrowing.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance.

Fixed income

Fixed income

Global government bonds were up 1.4% in February as investors became more cautious due to geopolitical risks, concerns about economic disruption from AI, and signs of labour market weakness in the US and UK. Falling inflation increased expectations of future interest rate cuts, particularly in the UK, where gilts performed strongly ending the month up 2.5%. US Treasury yields declined as markets priced in further policy easing later in the year. In contrast, corporate bond markets underperformed, with the gap between investment‑grade and high‑yield bond yields widening as investors demanded greater compensation for risk.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance.

Source: Quilter as at 28 February 2026. Total return, percentage growth over period 31 January 2026 to 28 February 2026. Equities are represented by the appropriate MSCI index, the Magnificent Seven is represented by the Roundhill Magnificent Seven ETF, UK gilts is represented by the ICE BofA UK Gilt Index, US Treasuries is represented by the ICE BofA US Treasury (GBP Hedged) Index, global government bonds is represented by the Bloomberg Global Aggregate Government - Treasuries (GBP Hedged) Index, and global corporate bonds is represented by the Bloomberg Global Aggregate - Corporate (GBP Hedged) Index.

The performance figures shown refer to past performance. Past performance is not a reliable indicator of future performance.

Marcus Brookes

Chief Executive Officer and Chief Investment OfficerMarcus is both the Chief Executive Officer and Chief Investment Officer of Quilter Investors. Marcus joined Quilter Investors in December 2021 from Schroders Personal Wealth, where he also held the role of Chief Investment Officer. Marcus has considerable investment management experience with a deep understanding of the multi-asset sector, having managed multi-manager fund ranges for more than 25 years at Schroders, Cazenove Capital, Gartmore, and Insight Investments.

Important Information

The value of investments can fall as well as rise. You might get back less than you invested.

This communication is issued by Quilter, a trading name of Quilter Investment Platform Limited.

Approver: Quilter March 2026

QIP 23842/29/15597