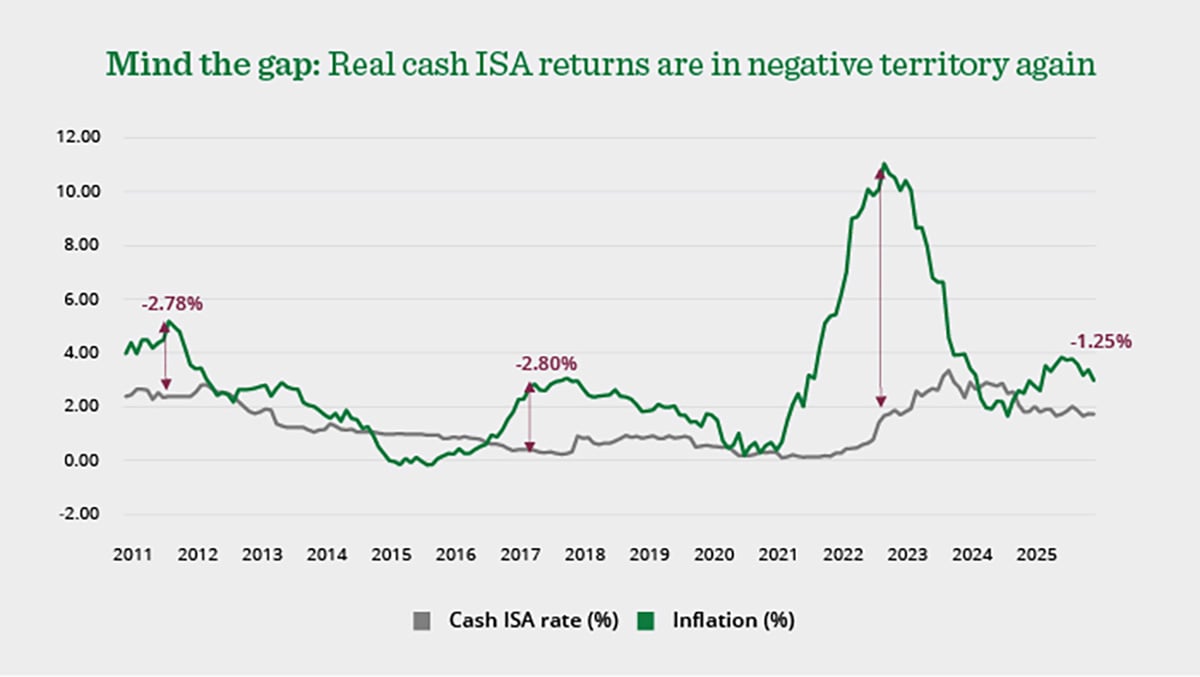

Savers have been losing money in real terms for 15 consecutive months (up to January 2026), as cash ISA and instant access savings rates continue to trail behind inflation.

While CPI inflation reached 3.0% in January 2026, cash ISA rates have barely shifted - locking in real‑term losses for millions.

Quilter’s latest analysis shows:

- Cash ISA rates have fallen by nearly a third (32%) since October 2024, the last time they kept pace with inflation

- Average instant access savings accounts are delivering a real‑terms loss of 0.85% a year

- £300bn is currently sitting in accounts paying no interest at all, leaving savers fully exposed to inflation.

With global uncertainty putting upward pressure on inflation again, the gap between prices and savings returns looks set to continue.