The page you were trying to view is not available for your role.

Summary

The latest blog from Sacha Chorley analyses the implications of recent political events and economic indicators in the UK, focusing on the Makerfield by-election and its potential effects on markets and investment.

1 to 9 Odds

I drew Australia in the World Cup sweepstakes with my friends. With bookies offering 500/1 on Australia to win the Cup, this is possibly the worst outcome for my own chances: not good enough to compete for the top prize, but not bad enough to challenge for the wooden spoon. As an England supporter, there is some consolation in England’s stronger position 9/1, reinforced by a solid 4–2 win over Croatia in their opening game.

It feels like a similar story in the Makerfield by-election. It has been confirmed that Andy Burnham has won the seat, in line with prediction markets, which had priced in around a 90% probability of victory the night before (roughly 1/9 odds).

Given the result was in line with expectations, it’s not surprising that the initial reaction in bond and equity markets has been muted. While the immediate response is always worth noting, we should not expect any material shift in the political landscape in the near term. Burnham’s path to Number 10 remains uncertain. Whether he is effectively coronated or faces a full leadership contest, it will take time for him to establish himself.

That being said, we should expect a little bit of increased volatility in the market: especially choppier moves in gilt yields and the pound as the political manoeuvres take place. Beyond that, it is worth trying to examine the investment drivers for UK investment assets over the medium term to understand what these results could mean.

From a fixed income perspective, it’s worth remembering that the UK has historically been seen as more sensitive to exogenously driven inflation spikes. In part this has been why UK bonds yields have risen more than, say, US yields since the start of the Iran-US conflict. More recently, it has been interesting that UK inflation has surprised on the downside of late – headline inflation printed 2.8 percent year on year for May, lower than expectations of 3 percent . While wage pressures remain, the newly signed memorandum of understanding (MOU) between Iran and the US, suggests nearer term inflation pressures are softening.

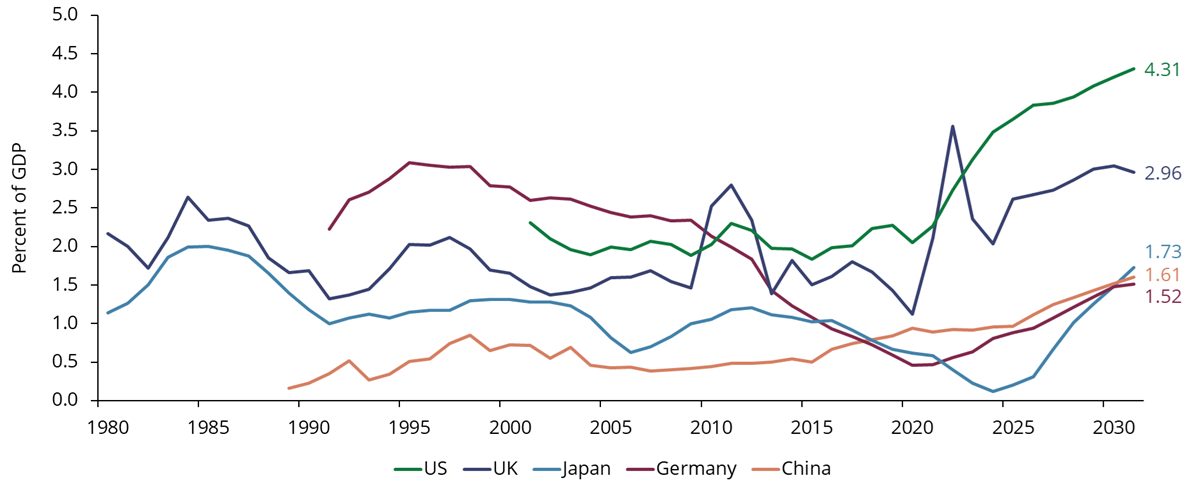

All this is significant because of the importance of the bond market to the plans that our politicians are trying to make. Defence spending in particular, is at the top of everyone’s agenda and Andy Burnham has expressed intentions to increase spending commitments (in targeted areas). This will require fiscal credibility: and therefore, it will be very important to understand who would be Chancellor in a Burnham-led government. Debt service costs (as a % of GDP) are already near all-time highs (although not as high as in the US!) and given that we have a much higher proportion of debt that is inflation-linked than others, we can’t even just inflate our way out of our debt problem.

General government interest expense (percent of GDP)

Source: Quilter, IMF, Macrobond as at 19 June 2026. General government interest expense as a percentage of GDP over period 1 January 1980 to 1 January 3031. Data for 2026 onwards is an estimate.

One obvious route

To improve the spending capacity of the economy is to promote growth. But here, the UK is a laggard (especially in terms of GDP per capita growth) and some of the comments from Burnham suggest that he has some fresh ideas to try to boost the productivity of the country. This would be welcome: the equity market has been down on domestically focused UK stocks for some time now with domestically focused stocks underperforming international exposure by around 10 percent since the start of the year and hitting decade lows of relative performance.

Some of the best performance from domestic stocks was in the period 2011-2015, with strong returns from the housebuilders and associated sectors. This was partly a reflection of the Help to Buy policy implemented by the Conservative government in 2013/14. Given the fiscal constraints Burnham will face if he manages to get to Number 10, it is unlikely that we will see any policy announced that would have as direct an effect on UK stocks.

Now it is a bit of a waiting game as we watch to see how Keir Starmer reacts to the news of Burnham’s election win. In his victory speech, Burnham reflected on how we need a bit more hope for the future. It’s interesting that Greater Manchester’s GDP per capita has outperformed the UK more widely since Burnham was elected Mayor. Perhaps then there is hope that this does mark a ‘turning-point’ for domestically focused UK assets although I still won’t hold out much hope for my chances in the sweepstakes.

Key takeaways

- Political shift – but no immediate market impact

- The Makerfield result was largely expected, so markets have reacted calmly rather than dramatically

- Any real change will take time, particularly while leadership questions and policy direction play out

- Short-term volatility, not a structural shift

- Some near-term volatility is likely - particularly in gilt yields and sterling - as political uncertainty unfolds

- But there’s no clear catalyst yet for a sustained change in the UK’s investment outlook

- Growth is the real long-term swing factor

- The UK’s challenge remains weak productivity and growth, which is weighing on domestic equities

- If policy can genuinely boost growth, there’s potential upside for UK-focused assets - but fiscal constraints make this harder to deliver

Sacha Chorley

Portfolio ManagerSacha is a portfolio manager of the Quilter Investors Cirilium and Creation Portfolios. Prior to joining Quilter Investors in 2011, Sacha worked at Broadstone with their team of economists before moving into asset allocation and fund manager research.

Sacha is a CFA charterholder and has also completed the Chartered Alternative Investment Analyst qualification. Sacha has a degree in Maths from the University of Bath.