The page you were trying to view is not available for your role.

1. Introduction

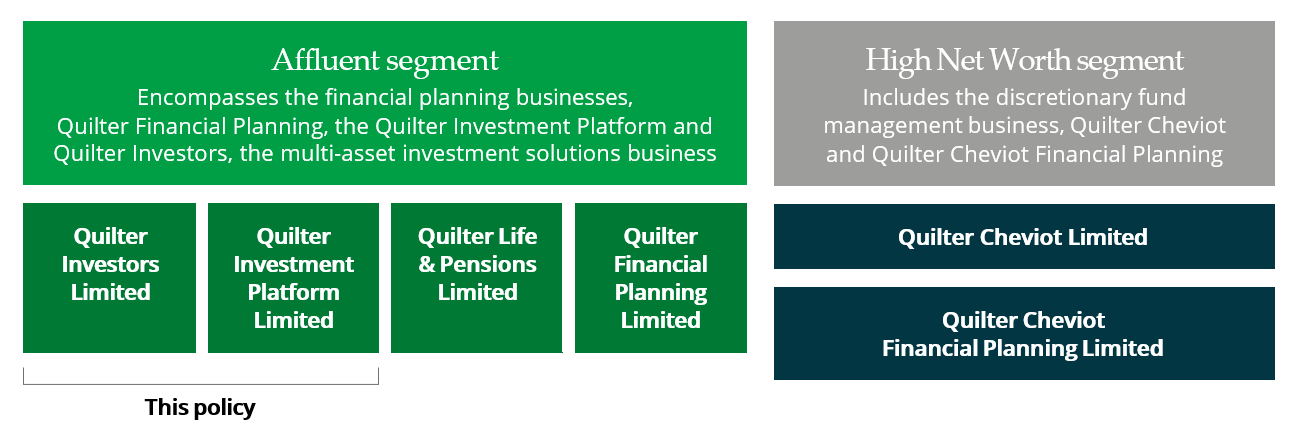

Quilter plc is a wealth management business that offers a range of investment services. It operates via two segments – Quilter Cheviot focusing on the High Net Worth segment and Quilter focusing on the Affluent segment. This Order Execution Policy covers the dealing process for the Quilter Affluent segment in relation to the funds which Quilter Investors oversees.

Quilter Investors Limited (QIL) is authorised to manage UCITS funds; is an Alternative Investment Fund Manager (AIFM) under the Alternative Investment Fund Managers Directive (AIFMD) and the Alternative Investment Management Regulations (as they apply in the UK) authorised to manage alternative investment funds, and is authorised to manage portfolios of investments in accordance with mandates given by investors on a discretionary client-by-client basis.

QIL invests in various asset classes including equities, fixed income, foreign exchange, exchange traded derivatives, and over the counter derivatives.

Quilter Investment Platform Limited (QIPL) undertakes some investment activities, including dealing, on behalf of QIL.

2. Scope

2.1 Entities

This policy applies to (i) QIL and (ii) QIPL where QIL has delegated the investment management activity of its funds to QIPL. As highlighted in the diagram below both firms form part of the Quilter Affluent segment.

Additionally, QIL, in its role as an authorised fund manager, requires appropriate execution policies are in place where execution has been further delegated by QIPL. These policies are reviewed periodically, and at least annually.

2.2 Activities

The investment management activities covered in this policy include the generation, execution and transmission of orders. Regulation explicitly requires us to act in the best interest of our clients and to take all sufficient steps to ensure we achieve and maintain the best execution of orders. This Order Execution Policy outlines the dealing arrangements through which we achieve best execution for our clients in respect of the trades we undertake for QIL’s multi-asset funds.

2.3 Instruments

This Order Execution Policy applies to any financial instruments which are covered by the UK’s Markets in Financial Instrument Directive (MIFID II). These include:

- Transferable securities

- Financial derivatives

- Contracts for difference

- Units in collective investment schemes

- Money market instruments

We trade on behalf of professional clients only for the activities referenced in this policy.

3. Governance structure

The following governance structure is currently in place for the orders we execute:

- Dealing Team: Responsible for best execution

- Senior Management Function Holder: The Director with Senior Management Function responsibility ensures that the QIL Order Execution Policy and execution arrangements are appropriately designed, implemented and maintained to enable QIL to obtain the best outcome for the execution of orders on QIL funds.

- Governance Forum: The appropriate governance forum monitors the execution outcomes achieved by the dealers and execution methods, independently of the dealers and broader in nature, and for ratifying the execution methods used.

- The Second Line are responsible for providing oversight on adherence to the Order Execution Policy expectations and it reports summary information to the SMF holder and appropriate fora.

4. Best execution

4.1 Order Generation

We operate a single investment desk. The investment desk routes their orders to the central dealing desk for execution.

We employ fund managers who are responsible for fund performance and to that end they generate orders to manage the fund assets of the relevant fund. Dealers are responsible for the execution or transmission of those orders to the relevant markets and for the selection of the counterparty and / or the execution venue. When authorising orders, the fund manager selects an associated execution benchmark which indicates the relative importance of some of the execution factors to the dealer.

Example execution benchmarks include:

- timed trades for execution at a specific time

- average daily market prices

- the current market

4.2 Execution and Transmission

Execution is where the dealer retains discretion to select the price achieved for an order and the trade is executed directly on a trading venue. For these executions we owe the client a duty of best execution.

For transmitted orders, the dealer passes some or all of the order pricing discretion to the counterparty and the associated duties of best execution travel with it. The transmission may include constraints or parameters within which the counterparty must work.

Where we transmit an order, the receiving counterparty owes us a duty of best execution. However, we retain an overarching duty of best execution to the client and the best interests of the client are supported through the selection of the most competent counterparty for the order and subsequent oversight reviews.

4.3 Order Placement

We employ experienced dealers who have ready access to the fund managers in the office and remotely. This arrangement facilitates communication which enhances the order execution process when the dealer needs to consult with the fund manager on execution factor priority.

It is important when placing a trade that the dealers have access to relevant pools of liquidity, counterparties and systems to ensure that the execution is transacted on the best possible terms. Dealers understand that the total cost of an execution includes both implicit and explicit costs. Although commission is an important component of that cost, market impact can be much greater if it is not acknowledged and managed.

The dealers will give priority to execution methods which match willing buyers and willing sellers (natural liquidity). These methods should offer the best execution outcome and reduce or eliminate the market impact.

Where natural liquidity is not available the dealers call on their experience to decide the optimum trading approach after taking all relevant factors into consideration.

4.4 Execution factors

When a dealer receives an order, they consider the characteristics or execution factors associated with the order together with the selected execution benchmark in order to determine the execution approach.

The execution factors include:

- price

- suitability of available venues to achieve the best execution price

- costs including explicit commissions and implicit market spreads or impact

- speed and likelihood of execution

- likelihood of settlement

- size and liquidity available in the instrument

- the nature of the

We determine the relative importance of these factors according to the following criteria:

- the objectives, investment policy and risks specific to the fund

- the characteristics of the order

- the characteristics of the financial instrument

- the characteristics of the execution venues to which that order can be directed.

In all cases the dealer selects an approach with the objective to achieve the best possible execution outcome taking into account costs and other execution factors. The importance of each factor varies for each order and the prevailing market conditions. Generally, price is the most important factor and when other factors are important, price remains important, subject to those other factors.

For timed orders, the importance of the speed of execution at the appropriate time is given importance. For market average orders, the commission rate paid for the service is the deciding factor subject to the ability of the counterparty to achieve or provide the market average price.

The size and liquidity factors are linked. For order sizes which are smaller than the available liquidity over the required timeframe then order size is not a limiting execution factor. Where the order size is larger than the available market liquidity, under some dealing approaches, the order could drain the market of liquidity and move the market price against the incomplete order. For such orders there is usually a compromise between time and size. If the fund manager allows more time for the execution, then the dealer may partially execute the order which may allow time for liquidity to recover before executing subsequent portions of the order.

For equities, the market capitalisation has bearing on the execution. Instruments with a large market capitalisation tend to have more market participants, trading more regularly and in larger size. Additionally, order sizes as a proportion of the market capitalisation are small. For most large capitalisation instruments, order size is manageable either using available market liquidity or with a short extension of the order time frame.

For medium and smaller capitalisation equities, there are relatively less market participants, trading less frequently and in smaller size. Order sizes can be material proportions of the market capitalisation. For small capitalisation orders, extending the order time frame and careful selection of the counterparty for their discretion and knowledge of the instrument become important factors for achieving the best overall price.

Where the fund manager requires a prompt execution, the dealer promotes the importance of the speed of execution factor. If the market is not able to absorb the order, then this may mean compromising on other factors in order to achieve the prompt execution. The dealer and the fund manager consult on the judgement for the size of the factor compromise.

For funds which require daily rebalancing, dealers typically select a timed or market average price approach. This achieves the execution within the necessary timeframe at the prevailing market level. Where such orders are collected together for execution as a package then the dealers select a program trade approach.

Program trades are also used to implement asset allocation changes where a fund manager wishes to switch a number of positions at the same time or to invest or divest the fund against client cash flows without destabilising the fund position.

The time is more flexible for funds which use a stock selection investment strategy. The dealer may be given more discretion to wait for the right market conditions or sources of natural liquidity in order to achieve a better price than the prevailing market level adjusted for the order size. Working the order over time will reduce the market impact but at the expense of running market risk during the execution.

For other orders the time factor may be uprated to ensure execution before a specific event or as a fast reaction to a recent event which is moving the market.

4.5 Best Execution over the long term

The regulatory requirement is that we take all sufficient steps to achieve the best possible outcomes on a consistent overall basis. Within this there may be individual executions which do not achieve the best possible result.

Quilter Investors has established alternative dealing arrangements with Northern Trust which will be utilised at our discretion for normal dealing activity and in particular for disaster recovery or business continuity scenarios, to support the continued execution of orders. Quilter Investors remain responsible for monitoring and overseeing the delegated execution.

5. Counterparty and Execution venue selection

We aim to select execution venues that enable the best possible result for the execution of client orders on a consistent basis. Venues are reviewed on a periodic basis by the appropriate governance forum.

We use counterparties which are regulated, either by the Financial Conduct Authority or by the counterparty’s home state regulator and are approved internally via our counterparty approval process.

The overriding consideration when selecting an execution venue or counterparty is that the venue or counterparty concerned has adequate systems and controls in place to enable the delivery of best execution.

Before executing an order, the dealers review the order execution factors to determine the candidate execution venues or counterparty and the execution methods to use.

5.1 Equity

For most types of equity orders, the first choice for execution venue are sources of natural liquidity. Larger orders in small and infrequent trading instruments may wait for natural liquidity over an extended period. During such a period the dealer regularly consults with the fund manager to assess the balance of the execution factors.

If there is no natural liquidity available, the dealer researches market liquidity trying to identify counterparties which have advertised an interest or recent activity in the instrument. This and other market colour may inform the dealer of execution venues which should provide the keenest prices for the order.

5.2 Fixed Income

Fixed income is largely an over-the-counter market. Execution may take place on electronic platforms or through direct communication between the dealers and counterparties. The trading activity for fixed income markets is concentrated in the largest banking counterparties.

For all fixed income trades and prior to dealing, the dealer researches a fair market level and liquidity for the transaction given the nature of the instrument, size, immediacy of the order and prevailing market conditions. The dealer uses this research to guide the selection of an execution method which may use either a manual or electronic approach, or a combination of both.

The electronic platforms we use are authorised as multilateral trading facilities (MTFs). Some MTFs provide competitive access to the more liquid segments of the fixed income market and typically facilitate a Request for Quote dealing process with the main counterparties offering liquidity in the instrument. Where the MTF restricts the number of price requests for a single order, the dealer selects candidate counterparties from their market pricing and size indications, together with any market colour and previous execution performance. Other MTFs are

peer-to-peer crossing networks which facilitate the identification of natural liquidity.

For manual orders, the dealer researches the instrument to identify the candidate counterparties and places them in competition for the order. Counterparty selection priority is given to counterparties indicating the best market prices for the size of trade as well as previous liquidity experience or indications of interest from market colour.

In competition, the dealer will endeavour to obtain a minimum of three executable prices which are within tolerance of the fair market spread level of prices shown on the order screen before executing. Where three such prices are not available the dealer may exercise judgement to determine if one of the available prices is within tolerance of the fair market spread level for prevailing trading conditions, order characteristics and immediacy of execution.

For larger orders the dealer may elect to work on a discrete basis with a single counterparty in order to minimise information leakage and market impact.

5.3 Exchange Traded Derivatives

We appoint clearing brokers in relation to exchange traded derivative transactions. A clearing broker is a member of multiple derivative exchanges and acts as the agent for the mandate executing and clearing exchange traded derivative transactions.

When executing an exchange traded derivative trade, the dealing desk will get a price quote from a variety of counterparties on the approved counterparties list and execute with the best price on each occasion. If the broker selected is not the appointed clearing broker, the trade is given up to our clearing broker.

5.4 Over The Counter Derivatives

As with exchange traded derivatives, we appoint clearing brokers in relation to cleared over the counter derivative transactions.

We execute over the counter derivative transactions with approved counterparties, providing a sufficient range of counterparties available to the dealers for selection.

Execution of cleared over the counter derivative transactions follows the same approach as fixed income execution. This involves assessing the expected fair market level, sourcing liquidity and where possible getting multiple competing quotes or working discretely with a single counterparty. These instruments are executed purely based on best price. The dealers obtain prices with approved counterparties and trade with the best price available.

5.5 Spot and Forward Foreign Exchange

The trading activity for foreign exchange markets is concentrated in the largest banking counterparties and we select counterparties from this group of banks. In addition, there are regional banks which specialise in currencies within their region. MTFs provide competitive access to these banks. FXall is the MTF used for this purpose and, the dealer selects candidate counterparties from their pricing history and performance, together with any market colour or regional strength.

We use the MTF to execute foreign exchange orders which facilitate a request for quote process from multiple counterparties simultaneously.

For some markets local regulation restricts the ability of a non-local investment firm to transact foreign exchange in the local currency. We delegate foreign exchange transactions in these markets to the fund’s custodian which does have the necessary local market relationships.

We also delegate some transactional foreign exchange and all share class hedging to the custodian with standard dealing terms agreed in advance.

5.6 Collective Investment Schemes

Transactions in collective investment schemes (CIS) are executed with the fund provider at the official price, at the next available Net Asset Value (NAV) point.

The portfolio manager selects the fund, the currency and the share class, then the desired CIS is routed through an electronic handling agent.

It does not go through the dealers, as such there is no price discovery to be sought by the Dealing Desk.

The majority of CIS have a single dealing price, normally generated around the NAV of the scheme.

All orders have to be placed before a specified dealing cut-off time which is typically shortly before the NAV point and varies from CIS to CIS.

5.7 Deposits

Generally, we are an active manager with portfolios that are typically fully invested with minimal residual cash balances however the portfolio manager has full discretion over the cash allocation invested in the funds. The cash on deposit is maintained at the custodian for our funds.

6. Program trades

The use of program trading is both an operationally and cost-efficient method to execute a list of securities under a single instruction. Counterparties agree to execute the list of securities against the specified benchmark for a commission rate determined in competition. It is a particularly useful method for managing client cash flows and asset allocation changes which give rise to batches of trades which must be executed promptly at the prevailing market level.

In a principal program trade, the counterparty agrees to execute the list of securities exactly in line with the agreed execution benchmark. The counterparty carries the risk of the execution against the benchmark and charges a commission appropriate for the risk. In an agency program trade, the counterparty works to achieve the agreed execution benchmark but does not guarantee to achieve it. In this case the risk the counterparty does not achieve the execution benchmark remains with the fund and therefore the commission rate is lower than for a principal program trade. For agency program trades it is paramount that the broker selected is able to control the market impact of the program trade and achieve the execution benchmark.

7. Agency crossing

An agency cross is where one fund passes a position to another fund. The price is set at a level which is beneficial to both sides of the cross, typically the market mid-price or a benchmark level. The execution is put through an independent counterparty or MTF. The transaction includes a fee to cover the counterparty or execution platform administration and facilitation cost.

8. Commission rates

The rate of commission for executing trades is dependent on the following factors:

- Asset class

- Execution venue

- Individual markets

- Transaction type

We do not participate in any commission recapture programmes because such programmes may conflict with the principles of best execution and therefore the best interests of our clients.

Commission levels are lower for electronic executions in comparison to executing the same order manually.

Fixed income and foreign exchange transactions tend to be executed on a principal basis with zero commission. Counterparties are remunerated via the bid-offer spread with the dealers ensuring such spreads are not excessive.

Equity trades are typically executed within a range of commission rates, with the level dependent on the market concerned and the associated market costs.

The distinction between program and single stock orders also affects average commission levels. Agency program trades attract a relatively low commission charge in comparison to program trades executed on a principal basis. Single stock orders tend to attract higher commission rates than agency program trades.

Orders in emerging markets tend to attract a higher commission charge than those in developed markets. This is due to a lack of market transparency, limited broker access, local market structure and therefore the higher associated costs of trading and settling transactions.

Futures contracts are traded and cleared using an existing flat charge per contract. We do not use commission sharing agreements.

9. Execution monitoring

The dealers are the specialists with the most in-depth knowledge of the markets and methods of execution. Therefore, the dealers are responsible for achieving and improving the best execution of the orders they execute.

The accountable senior management function (SMF) holder has the responsibility to seek to improve execution outcomes. Both the dealers and the accountable SMF holder monitor developments in the execution landscape to take into consideration the emergence of new venues, counterparties, functionalities and services.

Execution analysis reports are provided to the appropriate governance forum on a periodic basis (but no less than quarterly), to ratify the effectiveness of existing execution arrangements and to identify potential improvements. We also review execution reports from sub-advisors quarterly and escalate findings to the accountable SMF holder, as required.

10. Counterparty approval process

Only counterparties on the approved list may be used for a transaction. Before a potential counterparty can be used, due diligence is completed. This is initiated by a request from the dealing desk asking for the process of setting up a new counterparty to begin. This is followed by approval on several criteria including:

- Terms of business / Legal risk

- Compliance risk

- Financial risk

- Operational risk

Once this process is completed and all risks investigated, the final approval is given by the accountable SMF holder. The counterparty is then added to the approved list and set up as an approved broker within the order management systems.

11. Order allocation, priority and timely execution

No preference is given to any of the broad groups of clients or any one client over another.

All client orders are pre-allocated by the relevant fund manager within the order management system prior to being sent for execution. In instances where orders are partially filled, such fills are automatically allocated pro-rata by the order management system.

Post execution reallocations are only permitted in the instance of trade errors or where initial public offerings (IPO) or fixed income new issue allocations are deemed as uneconomical to clients. New and outstanding orders for the same stock are treated with equal priority. When a new order arrives on a dealing desk for a stock in which there is an existing unexecuted component then any partial execution is booked out and the remaining order component merges with the new order component. The dealer then re-presents the merged orders to the market as a single new order.

We have procedures in place to ensure orders are picked up and assessed promptly by the dealers to ensure their timely execution. As standard, dealers must acknowledge and place orders in the market in a prompt, fair and expeditious manner, subject to market opening times.

Where market conditions mean it is not appropriate to place orders promptly, the dealer may elect to delay placing the order in the market.

The order management system records the order history with timestamps for each appropriate action. The system retains the historical data in line with regulatory requirements.

The fund manager places all subscriptions for IPOs and underwritings on the order management system as per any other trade and these are processed in the same way. The order management system automatically calculates and allocates partially filled orders on a pro-rata basis.

New issues in IPOs and fixed income markets are regularly over-subscribed and allocations scaled back. Fund managers do not inflate new issue orders beyond the point of genuine portfolio demand in order to receive a better allocation. The order management system automatically allocates scaled back orders pro-rata subject to minimum issue sizes and de minimis allocations.

12. Stop lists

Where we receive price-sensitive information on a particular stock, this stock and any related instruments are placed on the relevant stop list, maintained and controlled by the Investment Controls team within the order management system, preventing funds from transacting in those instruments.

13. Information to clients

This Order Execution Policy forms part of the investment management agreement with our clients. By entering into an investment management agreement, the client accepts this Order Execution Policy including the possibility that some orders may be executed off venue, (see Appendix 1 for the list of venues).

Copies of this Order Execution Policy are available on request.

14. Inducements and conflicts of interest

We operate a robust inducements policy and do not pay or receive any fees or services, related to the investment service it offers, which do not benefit the client or conflict with the best interests of the client.

We also have a Conflicts of Interest Policy, copies of which are available on request.

15. Fast markets

In order to achieve best execution for clients, normal trading is expected to be restricted to normal market hours relative to the particular market in question.

However, there may be occasions that fast-moving markets outside of their usual market hours require trading to take place by exception. This is expected to be on very limited occasions and not for use in normal market conditions. We have no set triggers or limits due to market circuit breakers and other conditional restrictions that exist within markets that may mean we cannot respond in the interest of our customers.

Hence, a portfolio manager can on such occasions, submit orders and instructions to the dealing desk outside the normal UK office hours, but these must be made through monitored devices i.e. recorded mobile devices, emails, Bloomberg chats and deal tickets created in the order management system as usual, with no exceptions.

16. Policy review

The Head of Dealing reviews this policy annually with any material changes presented to the appropriate governance forum for approval. If any material changes are proposed outside of the annual review, these changes are also presented to the appropriate governance forum.

The review assesses this policy and execution arrangements in order to ratify that it is reasonably designed to enable us to obtain the best outcome for the execution of client orders. The review includes the addition or removal of execution venues or entities and any modifications to this policy, including the relative importance of the execution factors.

A material change means a significant structural change within Quilter, market or any regulation which would alter the relative importance of the execution factors or produce execution outcomes inconsistent with this existing policy. Any material changes will be reflected in the policy available on the client website on a timely basis.

We will make regular non-material adjustments to this policy, as and when required, including changes to counterparty and venue lists.

Any non-material changes, post the annual review undertaken by the Head of Dealing, do not require appropriate governance forum approval (e.g. amendments to counterparties).

17. Appendix 1 – Venues and counterparties

|

Equities including Investment Trusts |

|

|

Bank Of America Merrill Lynch Limited |

JP Morgan Securities Plc |

|

Cenkos Securities Plc |

Northern Trust Securities LLP |

|

Deutsche Numis Securities Ltd |

Panmure Liberum Capital Ltd |

|

Forte Securities Limited |

Singer Capital Markets |

|

HSBC Bank Plc |

Virtu Financial Ireland Limited |

|

Investec Bank Plc |

WBS Solutions Ltd |

|

Jefferies International Ltd |

|

|

Fixed Income |

|

|

Forte Securities Limited |

Virtu Financial Ireland Limited |

|

Northern Trust Securities LLP |

TD Securities Ltd |

|

Foreign Exchange |

|

|

Citigroup Global Markets Ltd |

Morgan Stanley & Co. International plc |

|

Goldman Sachs International |

Royal Bank of Scotland plc (NatWest) |

|

HSBC Bank plc |

Toronto Dominion Bank, Toronto |

|

JP Morgan Securities plc |

|

|

Exchange Traded Derivative - Clearer |

|

|

Merrill Lynch International |

|

|

Exchange Traded Derivative – Executing Brokers with Give Up Agreements |

|

|

Forte Securities Limited |

Merrill Lynch International |

|

Goldman Sachs International |

Northern Trust Securities LLP |

|

HSBC Bank plc |

|

|

Transition Management |

|

|

Citigroup Global Markets Ltd |

Northern Trust Securities LLP |

|

Multi-Lateral Trading Facilities |

||

|

Name |

Market Identifier Code |

Class |

|

Bloomberg Trading Facility Ltd |

BMTF |

Fixed Income |

|

FXall |

TRAL |

Foreign Exchange |